PCB Raw Material Costs in 2026

A PCB is a stack of distinct materials, each made by a different specialty manufacturer. The 2026 cost story is that almost every one of them has been formally repriced upward by its primary producer — copper foil, copper-clad laminate, glass fiber cloth, resin systems, gold, silver, palladium, tungsten carbide, solder mask ink, photoresist and process chemicals — inside a six-month window. This guide walks through every input material in order with the actual numbers from the manufacturers who set the prices, alongside the indicative cost ratios that determine what each one contributes to a finished PCB.

The market-level pricing context is in the PCB price increase analysis, supply-chain detail in the PCB material shortages analysis, AI-driven demand in the AI server PCB demand analysis, and design and procurement responses in the guide to reducing PCB costs.

1. The Full Bill of Materials Inside a PCB

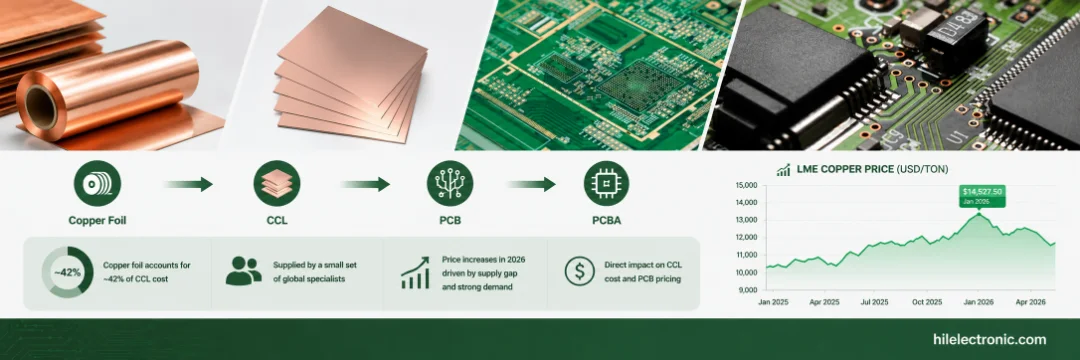

The cost stack inside a multilayer PCB is more layered than a casual breakdown suggests. Per TrendForce industry data, copper-clad laminate alone is the dominant material component of a multilayer board, and inside the CCL itself the cost decomposes approximately as copper foil 42%, resin 26%, glass fiber cloth 19%, balance ~13%. But CCL is only one of many inputs — the finished PCB also requires surface finish (with its own precious-metal exposure), drill bits, solder mask, photoresist, plating chemistry and process consumables.

| Material Category | Function in PCB | Share of Bare-Board Cost | Key Manufacturers |

|---|---|---|---|

| Copper-clad laminate (CCL) | Core dielectric with bonded copper foil. | 30-45% | Kingboard, Shengyi, Iteq, Resonac, MGC, Panasonic, EMC, TUC, Nan Ya, Doosan. |

| Copper foil | Conductive layers (input to CCL). | Inside CCL (~42% of CCL) | Mitsui Kinzoku, Furukawa, JX Nippon, Iljin Materials, Circuit Foil. |

| Prepreg | Resin-impregnated glass for layer bonding. | 5-15% | Same CCL makers as above. |

| Glass fiber cloth | Reinforcement inside dielectric. | Inside CCL (~19% of CCL) | Nittobo, Nan Ya, AGY, Asahi Kasei, Taiwan Glass, Baotek, Fulltech. |

| Resin system | Binds glass; sets Dk, Df, Tg. | Inside CCL (~26% of CCL) | Shengquan, SABIC, Asahi Kasei, MGC, Romira, Rogers, Taconic, Olin, Dow. |

| Surface finish (gold-based) | Solderable, corrosion-resistant coating. | 5-20% | Atotech, Rohm and Haas, Uyemura, MacDermid Alpha. |

| Tungsten carbide drill bits | Mechanical hole drilling. | 2-8% (5-8× on advanced) | Topoint, Union Tool, Zhongwu High-Tech, DingTai. |

| Solder mask ink (LPSM) | Solder-resist coating with photo definition. | 2-5% | Taiyo Ink, Resonac, Rongda, Guangxin Materials. |

| Dry-film photoresist | Patterning circuit features. | 2-4% | Asahi Kasei, Eternal Materials, Resonac, Chang Chun, Kolon, Mitsubishi Paper. |

| Plating & etching chemistry | Sulfuric acid, copper sulfate, etchants. | 5-10% | MacDermid Alpha, Atotech, Uyemura, Rohm and Haas. |

Material historically accounted for 30-50% of bare-board cost on multilayer PCBs. In 2026, with simultaneous repricing across copper foil, CCL, glass cloth, gold and tungsten carbide, the material share has moved toward 45-60% on advanced boards — the highest level in over a decade. Every category below has its own price story.

2. Copper Foil: The 42% That Drives Everything Else

Copper foil is the largest single input inside CCL (~42% per TrendForce). It is electrolytically deposited copper, typically 9-70 μm thick, made on dedicated production lines by a small set of global specialty producers. The 2026 price increases come directly from the manufacturers:

- Mitsui Kinzoku (Mitsui Mining & Smelting / 三井金属) notified customers on March 12, 2026 that all MicroThin copper foil products would rise 12% effective April 2026. Mitsui holds more than 90% of the premium-grade circuit copper foil market, including the HVLP-class foil used in advanced PCBs and IC substrates. In February 2026, Mitsui launched 3SAP-Ultra HVLP foil achieving Rz values below 0.5 μm for 12 μm thickness foil, targeting millimeter-wave 5G-Advanced and AI compute substrate applications.

- Mitsubishi Gas Chemical (MGC / 三菱瓦斯化学) announced increases of up to 30% across all product series including resin-coated copper foil, CCL and bonding sheets, effective April 1, 2026.

- Furukawa Electric (古河電気) and JX Nippon Mining & Metals — both major HVLP4 producers — raised prices 5-10% in Q4 2025 with continued adjustments into 2026. Both rank with Mitsui as the global HVLP4 leadership trio.

- Iljin Materials (일진머티리얼즈, South Korea) — major HVLP and RTF/VLP supplier — has similarly adjusted pricing.

- Circuit Foil (Luxembourg), Fukuda Metal Foil & Powder, Kingboard Chemical (vertically integrated standard foil), Co-tech Development (Taiwan), LCY Group (Taiwan, with HVLP4/HVLP5 below 0.4 μm Rz), and Jiangxi Copper (China, scaling HVLP5) round out the global supply base.

The underlying metal moved first. LME copper reached a record high of $14,527.50/metric ton in January 2026, 16.9% above the 2025 close, and stayed above $12,900/ton through early Q2 2026. According to industry analysis, the global HVLP4 capacity supply gap is projected at 500,000-600,000 kilograms per month starting mid-2026. The MLB (multilayer board) circuit copper foil market is projected to grow from approximately 15,000 tons in 2025 to 31,000 tons by 2028 and 54,000 tons by 2030, and per industry analysis orders for 2026 have already exceeded installed capacity at several producers.

| Foil Grade | Surface Roughness (Rz) | Typical Use | Cost vs Standard ED |

|---|---|---|---|

| Standard ED (electrodeposited) | ~7-8 μm | FR-4 multilayer, sub-1 GHz digital. | 1× (baseline) |

| RTF (Reverse-Treated Foil) | ~3-5 μm | High-Tg multilayer, entry high-speed. | ~1.3-1.5× |

| LP / VLP (Low / Very Low Profile) | ~2.5-4 μm | 10 Gbps+ digital, mid-loss laminate. | ~1.5-2× |

| HVLP (Hyper Very Low Profile) | <2 μm | 56G-112G channels, M6+ CCL. | ~2-3× |

| HVLP4 / HVLP5 | ~1 μm class and below | 224G channels, M7+, AI compute boards. | Premium & allocated |

The premium grades matter because of skin effect. At high frequencies current flows in a thin layer at the conductor surface, so rough foil lengthens the effective current path and raises resistive loss. Switching from standard ED foil (Rz ~7 μm) to HVLP (Rz <2 μm) improves insertion loss by approximately 5-8% above 10 GHz — on a 10-inch trace this can be a decisive 3 dB at the eye diagram. The ASP of high-end MLB circuit foil used in AI server and network equipment runs at more than 3× the ASP of battery copper foil and general-purpose mainboard substrate foil, with semiconductor packaging substrate foil priced at more than 10× standard general-purpose copper foil.

How does copper foil reach the PCB quote->

Copper foil flows into the PCB quote through CCL — bonded onto the dielectric core to form the conductive layer of every layer pair. The CCL maker buys foil from Mitsui, Furukawa, JX Nippon, Iljin or other suppliers, builds the laminate, and sells it to the fabricator. Mitsui’s 12% MicroThin increase and MGC’s 30% resin-coated foil increase both flow directly to the fabricator’s CCL purchase price before any drilling, plating or finishing.

3. Resin Systems: Epoxy, PPE/PPO, BT, PTFE

Resin is the chemistry that defines a laminate’s electrical and thermal personality. The resin choice separates standard FR-4 from high-Tg FR-4, from mid-loss laminates, from low-loss laminates, from RF/microwave-grade materials. Each resin family has its own producer concentration:

| Resin Family | Used In | Key Producers | 2026 Status |

|---|---|---|---|

| Standard epoxy | FR-4 multilayer. | Shengquan (圣泉), Olin, Dow, Nan Ya Epoxy, Kukdo Chemical. | Lead time extended; displaced PPO demand. |

| Modified epoxy (high-Tg) | High-Tg FR-4. | Same epoxy producers + specialty modifiers. | Tight; absorbing displaced PPO demand. |

| PPE / PPO | Megtron, I-Speed, M4-M7 mid/low loss. | SABIC, Asahi Kasei, MGC, Romira. | Production disruption at largest source. |

| BT (Bismaleimide-Triazine) | BT substrates, certain high-Tg laminates. | Mitsubishi Gas Chemical. | Tight; concentrated supply. |

| Hydrocarbon (low-loss) | M8+ ultra-low-loss CCL. | Rogers, Taconic, Arlon, Isola. | AI-driven allocation. |

| PTFE (pure) | RF, microwave, millimeter-wave boards. | Rogers Corporation, Taconic, AGC. | Specialty; premium pricing. |

The biggest 2026 resin story is on the PPE/PPO side. PPE provides the combination of low dielectric loss, high glass-transition temperature and dimensional stability that high-frequency PCBs require, and no other resin chemistry matches it at comparable cost. A production disruption at the largest single global PPE source in early April 2026 reduced effective supply substantially, with recovery projected over 6-9 months. Because the alternative PPE producers (Asahi Kasei, MGC, Romira) operate at materially smaller scale, they cannot absorb the gap quickly.

The propagation through other resin families is severe. PPE-based mid-loss laminate buyers have shifted orders to high-Tg epoxy laminates as a temporary substitute, absorbing epoxy capacity that would normally serve standard FR-4. Standard epoxy resin lead times have extended from approximately 3 weeks to 15 weeks. Shengquan Group (圣泉), a major Chinese epoxy resin supplier to the CCL industry, has been a direct beneficiary of the cycle as Chinese CCL makers turn to local resin supply.

What is PPE resin and why is it the 2026 PCB story->

PPE (polyphenylene ether), also called PPO (polyphenylene oxide), is a high-performance thermoplastic resin used as the backbone of mid-loss and low-loss PCB laminates including Panasonic Megtron 6/7 and Isola I-Speed. It is essential for boards running 5G, AI server, automotive radar and high-speed networking traffic. A production disruption at the largest single global PPE source in April 2026 reduced effective supply substantially, with no alternative producer at comparable scale. The result has been allocation of PPE-based laminates and propagation of tightness through the entire resin supply chain.

4. Glass Fiber Cloth: E-Glass, NE-Glass, T-Glass, Q-Glass

Glass fiber cloth is the reinforcement inside every CCL. Standard E-glass is widely available; the specialty grades that high-speed and AI-server PCBs require are not. The supply concentration is severe — Nittobo (Nitto Boseki / 日東紡, Tokyo Stock Exchange 3110) holds approximately 90% of the global T-glass market and 60-70% of NE-glass, per TrendForce industry analysis. Nittobo is also the world’s only company capable of stably mass-producing top-grade T-glass at scale.

Nittobo’s pricing actions therefore set the trajectory for the entire fine-weave glass segment:

- August 2025: Price increase of approximately 20% across the glass fiber product line.

- April 2026: Additional increase of approximately 20-30%.

- Capacity investment: Initial approximately JPY 15 billion (~$96-102 million) Fukushima 3× capacity expansion announced, expanded to a total approximately JPY 50 billion across 2026-2027 for Japan and Taiwan production. New facilities slated to come online from late 2026, with full impact by 2028.

- Nan Ya partnership (Nov 2025): Nan Ya Plastics (Formosa Plastics Group) will produce 20% of the specialty glass-fiber fabrics that Nittobo supplies to the global market by 2027. Nittobo will provide Nan Ya with long-term stable supply of glass yarn for Nan Ya’s second-generation low-Dk NER glass.

- Baotek (5340 TT / 健榮工業): Nittobo’s Taiwanese subsidiary currently produces high-end NE-glass on Nittobo-supplied glass fiber yarn, with 500-furnace capacity.

- Next-generation T-glass (2028): Nittobo plans an upgraded T-glass with coefficient of thermal expansion improved approximately 30% (from ~2.8 ppm to ~2.0 ppm).

T-glass has surged to approximately $100 per kilogram per industry sources, with orders backlogged into the following year’s Q2. Chinese electronic-grade glass-fabric producers are also raising prices — per industry reporting, Chinese fabric makers issued four successive price hikes across October and December 2025 and January and February 2026, with cumulative 2025 increases exceeding 50% and projections of monthly 10-15% increases continuing in 2026.

| Glass Grade | Composition | Effective Dk | Primary Suppliers |

|---|---|---|---|

| E-glass (standard) | Aluminoborosilicate | ~6.1 | Taiwan Glass, Nan Ya, AGY, Baotek, multiple. |

| NE-glass (low-Dk) | Low-Dk borosilicate | ~4.4 | Nittobo (60-70%), Asahi Kasei, Taiwan Glass, Fulltech, Taishan, Hong Ho. |

| T-glass (low-CTE) | Low-CTE specialty | ~5.0 | Nittobo (~90%), Taiwan Glass, Fulltech Fiber Glass, Hong Ho. |

| Q-glass (quartz fiber) | High-purity SiO₂ | ~3.8 | Shin-Etsu, Asahi Kasei, Glotech, Feilihua, Taishan, Hong Ho. |

The supply story behind these grades matters because high-speed signaling demands fine-weave, low-CTE glass. At 56G/112G/224G data rates, the woven fiber pattern itself introduces signal distortion (the “glass-weave effect”) — signals crossing fiber bundles see different effective Dk than signals crossing resin-rich pockets. Specialty glasses solve this. Q-glass (made from pure quartz fiber) goes further by lowering the dielectric constant itself, enabling the Df ~0.0007 performance that M9-class CCL achieves.

5. Surface Finish: Gold, Silver, Palladium, Tin, OSP

PCB surface finishes are based on real precious metals. The 2026 precious-metals market has moved sharply — spot gold reached an all-time high of $5,595.42/oz on January 29, 2026, traded at approximately $4,327/oz in mid-June 2026, and has averaged well above $4,000/oz across the year. Year-on-year this is approximately a 56% increase from the 2024-2025 baseline of approximately $2,600-$3,300/oz. J.P. Morgan Global Research projects gold reaching $6,000/oz by year-end 2026 with $6,300/oz possible in 2027.

Because gold accounts for approximately 70% of ENIG (Electroless Nickel Immersion Gold) process cost, the bare-board cost impact is direct:

- ENIG-finished bare-board costs up 5-30% depending on the gold area of the panel, with heavy-gold panels at the upper end.

- An additional approximately $40 per square meter on standard double-sided boards with heavy gold coverage, attributable purely to the gold component of the finish.

The leading surface-finish chemistry suppliers — Atotech (MKS Inc.), Rohm and Haas Electronic Materials (Dow), Uyemura International, and MacDermid Alpha (Element Solutions) — have all adjusted pricing in line with the underlying precious-metals market.

| Surface Finish | Composition | Cost per in² | 2026 Cost Pressure |

|---|---|---|---|

| HASL / Lead-free HASL | Tin alloy | Lowest among solderable finishes | Low — tin-led pricing. |

| OSP | Organic coating, no precious metals | Lowest overall | Minimal. |

| Immersion silver | Pure silver thin layer | $0.20-$0.40 | Moderate — silver-price exposure. |

| Immersion tin | Pure tin coating | Low-Moderate | Tin price exposure. |

| ENIG | Ni (3-6 μm) + Au (2-5 μin) | $0.30-$0.60 | High — 70% of cost is gold. |

| ENEPIG | Ni + Pd + Au | Premium | High — gold + palladium combined. |

| Hard gold / gold finger plating | Thick electroplated Au | Highest | Very high — thick gold layer. |

ENEPIG has gained share over ENIG in some applications because the palladium barrier layer allows a thinner gold top layer, partially offsetting gold-price exposure while improving wire-bond reliability.

How much has ENIG actually risen in 2026->

Gold itself rose 50-60% relative to the 2024-2025 baseline. Because gold is approximately 70% of ENIG process cost, ENIG-finished bare-board costs are running 5-30% higher depending on gold area of the panel. For standard double-sided boards with heavy gold coverage, the gold component alone has added approximately $40 per square meter beyond 2024 baseline. For high-gold-area panels (gold fingers, large pad area), the impact reaches the upper end of that range.

6. Tungsten Carbide Drill Bits and PCB Tooling

Almost all PCB mechanical drilling uses tungsten-carbide micro-drills. The global tungsten market hit a structural turning point with prices reaching approximately six times prior baseline levels. Industry analysts forecast 2026-2030 average tungsten carbide prices in the range of $450-$500 per 10 kilograms — a structural step-change from prior pricing rather than a temporary spike.

The major PCB drill manufacturers:

- Topoint Technology (尖點科技, Taiwan) announced its second 2026 price increase in Q1 2026 alone, extending from standard tungsten white drills to high-end products. Topoint signed a strategic cooperation agreement with Zhen Ding Technology in December 2025 for AI server and IC substrate PCB drilling. In May 2026, Topoint raised NT$600 million (~US$19.1 million) via convertible bonds, bringing in major PCB makers as strategic investors. Topoint targets 55% sales share in 2026 in high-end coated drills, with utilization already above 90% but still unable to fully meet demand.

- Union Tool (ユニオンツール, Japan) — the global technology leader in PCB micro-drills — has adjusted pricing aligned with tungsten carbide raw-material cost.

- Zhongwu High-Tech (中钨高新, China, 000657.SZ) launched a new nano-diamond-coated micro-drill specifically designed for M9-grade Q-glass substrates. Order book reported as fully booked. The company’s 140-million-unit micro-drill capacity expansion reached full production in March 2026, with additional expansion of 130 million micro-drills underway, plus 63 million extra-long, high-precision miniature cutting tools.

- DingTai High-Tech (301377.SZ), Wold Diamond Tools (688028.SH), Hengfeng Tools (300488.SZ), Huarui Precision, Xinrui Shares (688257.SH) — additional capacity ramping at the lower and middle of the market.

For 44-layer and 78-layer AI server PCBs with Q-glass substrates, drill consumable costs run 5-8 times traditional levels. Q-glass in particular is harder and more abrasive than standard E-glass, requiring nano-diamond-coated micro-drills that cost multiples of conventional ones and have shorter useful life per cutting edge. For these advanced boards, drill consumables are a meaningful component of the bill of materials rather than a back-of-envelope item.

Are drill bits really a meaningful PCB cost in 2026->

Yes — especially on advanced boards. On a standard 4-8 layer FR-4 board, drill consumables are typically 2-4% of bare-board cost. On a 22-layer high-Tg board, drill consumables can be 5-8%. On a 44-layer Q-glass AI server PCB, drill consumables run 5-8× standard levels, easily reaching double-digit percentages of the bare-board cost. Topoint and Zhongwu both report full order books and have implemented multiple 2026 price adjustments.

7. Solder Mask Ink, Photoresist and Process Chemicals

The “back-end” materials are easy to overlook because they sit inside the fabricator’s overhead. All have moved meaningfully in 2026.

Solder mask ink (LPSM, liquid photoimageable solder mask). Per QYResearch industry data, the global solder mask ink market is dominated by a small number of producers — Taiyo Ink (太陽インキ製造), Rongda Photosensitive Materials, Guangxin Materials, and Resonac together hold approximately 72% of the global market with Taiyo as the clear leader. Solder mask ink uses epoxy resins, photoinitiators and pigments — every input has seen cost pressure in 2026 — and Taiyo Ink has been expanding production capacity globally, including specialty inkjet solder masks for advanced PCBs and dielectric/conductive inks for solar, lighting and display markets.

Dry-film photoresist. Used to pattern circuit features during inner-layer imaging. Per QYResearch industry data, the top six producers hold approximately 67% of the global PCB dry-film photoresist market: Asahi Kasei (旭化成, with the SunFort™ dry-film line produced at the world’s largest dry-film coating plant in Suzhou plus Changshu), Eternal Materials (長興材料), Resonac, Chang Chun Group (長春集團), Kolon Industries (코오롱인더스트리), Mitsubishi Paper Mills. Additional players include DuPont, Qnity, Hunan Chuyuan New Materials and Hangzhou First Applied Material. Japan accounts for approximately 55%+ of global dry-film production; Asia-Pacific holds approximately 73% of the global market.

Process chemicals and plating chemistry. PCB plating, etching and surface preparation depend on consistent supply of electronic-grade sulfuric acid, copper sulfate, ferric chloride, ammonium persulfate and various other chemistries. The major formulation suppliers — MacDermid Alpha (Element Solutions), Atotech (MKS Inc.), Uyemura International, Rohm and Haas Electronic Materials (Dow) — formulate proprietary bath chemistries for copper plating, electroless nickel, immersion gold/silver and similar processes. Pricing has moved with input chemistry costs, and the global sulfuric acid market has tightened, contributing to upward pressure on electronic-grade chemistry pricing through 2026.

| Chemistry Category | Market Concentration | Key Suppliers |

|---|---|---|

| Solder mask ink (LPSM) | ~72% by top three | Taiyo Ink, Rongda, Guangxin, Resonac. |

| Dry-film photoresist | ~67% by top six | Asahi Kasei, Eternal, Resonac, Chang Chun, Kolon, Mitsubishi Paper. |

| Surface finish chemistry | Concentrated among four | Atotech, Rohm and Haas, Uyemura, MacDermid Alpha. |

| Copper plating chemistry | Concentrated | MacDermid Alpha, Atotech, Uyemura. |

| Etchants (cupric/ferric chloride) | Regional | Multiple Asian and Western suppliers. |

8. Real CCL Grade Pricing from FR-4 to M9

All of the above flows into CCL grade pricing — which is what fabricators actually buy. The cost progression up the laminate ladder is non-linear: each step changes resin chemistry, foil profile and glass type at the same time, multiplying cost rather than adding to it. Per Citi Research analysis, the average CCL selling price moved from RMB 150-160/sheet at end-2025 to RMB 180-190/sheet by mid-2026, with annual 2026 average forecast at RMB 220/sheet (+76% YoY) and year-end spot at RMB 240/sheet.

| CCL Grade | Df | Foil / Glass / Resin | Cost vs FR-4 | Example Products |

|---|---|---|---|---|

| Standard FR-4 | ~0.02 | Std ED / E-glass / Epoxy | 1× | Kingboard KB-6160, Shengyi S1141. |

| High-Tg FR-4 (Tg 170+) | ~0.015 | RTF / E-glass / Modified epoxy | ~1.2-1.4× | Shengyi S1000-2, Iteq IT-180A. |

| Mid-loss (M4 class) | ~0.010 | VLP / NE-glass / PPE | ~2-3× | Megtron 4, EMC EM-370. |

| Low-loss (M6 class) | ~0.004 | HVLP / NE-glass / PPE-modified | ~3-5× | Panasonic Megtron 6, Isola I-Speed. |

| Ultra-low-loss (M7) | ~0.0025 | HVLP4 / T-glass / Hydrocarbon-PPE | ~6-9× | Megtron 7, EMC EM-528, TUC Tachyon. |

| M8 class | ~0.0015 | HVLP4/HVLP5 / T-glass | ~10-15× | Doosan, Panasonic M8U class. |

| M9 (Q-glass) | ~0.0007 | HVLP5 / Q-glass / PTFE-hydrocarbon | ~15-20× | AI server midplane CCL. |

| PTFE / Rogers-type | ~0.001-0.004 | Specialty foil / PTFE | ~5-20× | Rogers RO4000/RO3000, Taconic. |

Within each grade, the major CCL producers compete on slightly different formulations. Kingboard, Shengyi, Iteq, EMC, TUC, Nan Ya, Doosan, Resonac, MGC and Panasonic each have product lines at multiple grade levels. The fabricator’s specific choice depends on the design’s Dk, Df, Tg, thermal and reliability requirements as well as material availability.

What is the most expensive base material on a PCB in 2026->

For digital boards, M9 Q-glass CCL used in AI server midplane and inference-rack designs, at roughly 15-20× standard FR-4. For RF and millimeter-wave designs, PTFE-based Rogers-type laminates at 5-20× FR-4 depending on grade. Among surface finishes, hard gold electroplated finger plating is the most expensive per unit area, but the laminate grade typically dominates the bill of materials for digital boards.

9. How the Material Stack Adds Up to Per-Square-Meter Pricing

All of the above flows into the per-square-meter price that end-customers see in a quote. Per industry reporting citing Victory Giant teardown data via Reuters, in 2026:

- Standard multi-layer PCBs: approximately $204 per square meter.

- High-end AI server boards: approximately $1,970 per square meter — nearly 10× the standard rate.

The 10× difference is material-driven: layer count, CCL grade, copper-foil profile, glass cloth grade, surface finish and via construction multiplied together. For an AI server board on M7+ CCL with HVLP4/HVLP5 foil, T-glass cloth, ENIG or ENEPIG finish and 22-44 layer construction, every input material sits at the premium tier of its category.

Procurement example: a 12-layer industrial telecom board specified on Panasonic Megtron 6 (M6 PPE-based CCL with HVLP foil and NE-glass) was quoted at three suppliers in late Q1 2026 with a 35% price range between the lowest and highest quotes. The cause was not supplier margin — it was different CCL allocations. The cheapest quote came from a fabricator with reserved Megtron 6 inventory from a 2025 forward order; the most expensive came from a fabricator quoting against spot. The procurement team awarded the middle quote, which came with a written CCL allocation confirmation, rather than the lowest one which carried a “material to be confirmed” clause.

Why does CCL allocation matter as much as price in 2026->

Because in a quota-and-allocation market, a price without confirmed material allocation is a guess. CCL makers including Kingboard, Shengyi, MGC, Resonac, EMC, TUC and Doosan have all moved to allocation-based supply in 2026, meaning each customer gets a defined monthly tonnage and new orders queue. A PCB fabricator without reserved CCL cannot promise a delivery date — and quoting on unsecured material risks both schedule slip and post-PO repricing if material has to be sourced at spot.

10. PCB Raw Material Cost FAQs

How much of a PCB’s cost is raw material in 2026

For multilayer PCBs in 2026, raw material has moved to 45-60% of bare-board cost, up from 30-50% in 2024, because copper foil, CCL, glass fiber cloth, gold and tungsten carbide have all risen sharply at the same time. AI server boards on M7+ CCL routinely hit the upper end; standard FR-4 boards are closer to 35-45%.

What is CCL and why does it dominate the 2026 PCB story

CCL (copper-clad laminate) is the core dielectric with bonded copper foil that forms every layer pair of a PCB. Per TrendForce, its cost breaks down approximately as copper foil 42%, resin 26%, glass fiber cloth 19%. With Mitsui Kinzoku +12% on MicroThin foil, MGC +30% on resin-coated foil, Kingboard four hikes in 2026, Iteq +20-40%, and Nittobo +20-30% on T-glass cloth, all three major CCL inputs have moved up at the same time.

Why did copper foil rise 12-30% in 2026

The underlying LME copper price reached $14,527/ton in January 2026 — a record high. Mitsui Kinzoku raised MicroThin foil 12% effective April 2026; Mitsubishi Gas Chemical raised resin-coated foil 30% effective April 1, 2026. Furukawa Electric and JX Nippon Mining also adjusted 5-10% from Q4 2025. Premium specialty foils (HVLP, HVLP4, HVLP5) rose further because their capacity is independently constrained.

What is HVLP copper foil and is it worth the cost

HVLP (Hyper Very Low Profile) copper foil has surface roughness below 2 μm Rz, versus ~7-8 μm for standard ED foil. It costs roughly 2-3× standard foil but improves insertion loss by 5-8% above 10 GHz — sometimes 3 dB on a 10-inch trace. It is generally required from 25 Gbps+ and necessary at 56 Gbps and 112 Gbps. Mitsui Kinzoku holds more than 90% of premium-grade foil supply; Mitsui’s new 3SAP-Ultra HVLP foil launched February 2026 achieves Rz below 0.5 μm.

What is PPE resin and why is it the 2026 PCB story

PPE (polyphenylene ether), also called PPO, is the high-performance resin backbone of mid-loss and low-loss laminates including Panasonic Megtron and Isola I-Speed. A production disruption at the largest single global PPE source in April 2026 reduced effective supply substantially, with no alternative producer at comparable scale. Recovery is projected at 6-9 months.

Why is T-glass fiber cloth a 2026 cost story

Because Nittobo holds approximately 90% of global T-glass supply, raised prices 20% in August 2025 and another 20-30% in April 2026, and its capacity expansion (3× by 2028, total ~¥50 billion investment for 2026-2027) does not produce material output until late 2026. T-glass has surged to approximately $100/kg with orders backlogged into the following year. Chinese fabric makers issued four successive price hikes Oct/Dec 2025 + Jan/Feb 2026, with cumulative 2025 increases above 50%.

What is the most expensive material on a PCB in 2026

For digital boards: M9 Q-glass CCL used in AI server midplane designs, roughly 15-20× standard FR-4. For RF and millimeter-wave: PTFE-based Rogers-type laminates, 5-20× FR-4. For surface finishes per unit area: hard gold electroplated finger plating; though laminate dominates the bill on digital boards.

How much has ENIG actually risen in 2026

Gold itself rose from approximately $2,600/oz in 2024 to a peak of $5,595/oz in January 2026 (+56% YoY). Because gold is approximately 70% of ENIG process cost, ENIG bare-board costs are running 5-30% higher in 2026. For panels with heavy gold coverage, the gold component alone adds approximately $40 per square meter beyond 2024 baseline.

Are drill bits really meaningful PCB costs

Yes — especially on advanced boards. Tungsten carbide prices stabilized in 2026 at 50%+ above 2024, with industry analysts forecasting $450-$500 per 10 kg average through 2030. Topoint Technology implemented two price hikes in Q1 2026 alone with utilization above 90%. Zhongwu High-Tech launched M9-grade nano-diamond drills priced at multiples of conventional ones. For 44-layer Q-glass AI server PCBs, drill consumable costs run 5-8× standard levels.

How can procurement reduce material price volatility

Four moves matter most in 2026: (1) submit a rolling 12-26 week forecast so the fabricator can reserve CCL allocation; (2) qualify a second CCL grade per board type; (3) use hybrid stackups that drop premium material on non-critical layers; (4) move to indexed pricing tied to a transparent copper-foil and CCL-grade formula. Combined, these convert spot-price shocks into a managed range.

Recommended Posts

Taconic RF-35 PCB Manufacturing Service — Prototype Through Volume Production

Figure 1. Taconic RF-35 PCBTaconic RF-35 is the workhorse...

Isola Astra MT77 PCB Manufacturing

Figure 1. Isola Astra MT77 PCB ManufacturingIsola Astra...

Custom Rogers RO4835 PCB Fabrication & Assembly Services

Figure 1. Rogers RO4835 PCBRogers RO4835 PCB is a...

Nelco N4000-13 PCB Material and Manufacturing Guide | Highleap Electronics

Figure 1. Nelco N4000-13 PCBNelco N4000-13 PCB is a...

How to get a quote for PCBs

Let’s run DFM/DFA analysis for you and get back to you with a report. You can upload your files securely through our website. We require the following information in order to give you a quote:

-

- Gerber, ODB++, or .pcb, spec.

- BOM list if you require assembly

- Quantity

- Turn time

For PCBA services, please provide your BOM (Bill of Materials) and any specific assembly instructions. We also offer DFM/DFA analysis to optimize your designs for manufacturability and assembly, ensuring a smooth production process.